A SaaS founder once posted on Reddit (r/netsec) that his company lost a $95,000 enterprise deal, despite having a SOC 2 report. The procurement team opened it, skipped to the auditor’s opinion section, saw two words, and flagged it.

The two words were “qualified opinion.”

If you have a SOC 2 report in hand right now, or you are working toward one, this distinction matters more than most founders realise.

A SOC 2 unqualified opinion tells every buyer and enterprise procurement team that your controls met the applicable Trust Services Criteria without material exceptions. A SOC 2 qualified opinion tells them something fell short.

Depending on the buyer, that could mean a delayed deal or a lost contract.

And the part that catches most people off guard is “Unqualified” sounds like a bad thing. It is not. In audit language, “unqualified” is the best outcome you can get.

Before your SOC 2 opinion becomes a buyer objection, fix the gaps early with ComplyJet. Start your readiness check for free!

Over 60% of enterprise procurement teams now require SOC 2 as part of vendor due diligence, and the opinion section is the first thing they read. Understanding what each outcome means and what to do about it is not optional anymore. In this article, we cover all the aspects of it.

If you want the short version before diving in, here it is.

SOC 2 Opinion Types at a Glance: 7 Things to Know

- A SOC 2 unqualified opinion is the best possible audit outcome. The auditor found no material issues with your controls. It is also called a clean opinion or an unmodified opinion.

- "Unqualified" sounds negative, but means the opposite. In audit language, "qualified" means the opinion comes with exceptions attached. "Unqualified" means none. It is a full, unconditional endorsement.

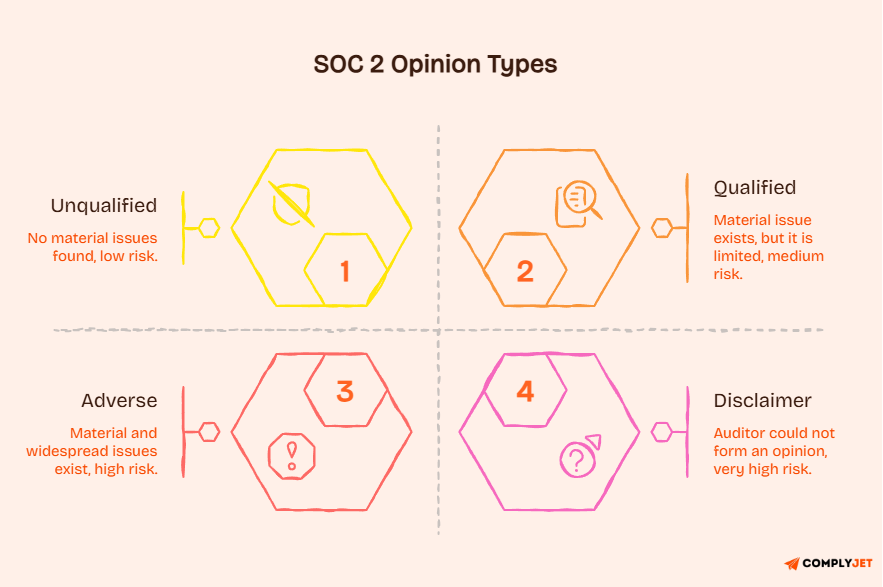

- There are four SOC 2 audit opinion types: unqualified (best), qualified (material issues, limited scope), adverse (material and pervasive issues), and disclaimer of opinion (insufficient evidence). Only the first is commercially viable.

- A qualified opinion is not an automatic vendor disqualification. Buyers should read the Basis for Qualified Opinion section to understand what failed and whether it affects their specific use case.

- Exceptions in a SOC 2 report are not the same as a qualified opinion. Most SOC 2 Type 2 reports contain documented exceptions. A qualified opinion only results when exceptions are material enough to impair a specific Trust Services Criterion.

- Adverse and disclaimer opinions are extremely rare. Most experienced SOC 2 auditors report never issuing one. The collaborative nature of the audit process prevents examinations from reaching these outcomes.

- In 2026, the opinion section is the first thing enterprise procurement teams check. A SOC 2 unqualified opinion signals program maturity and accelerates deal timelines, giving you a red signal. The governing standard is AICPA SSAE 18, updated by SSAE 21 (AT-C Section 205), effective June 15, 2022.

Now that the basics are clear. Let's get into the details.

What Is a SOC 2 Unqualified Opinion?

SOC 2 is not a certification, as many of you might’ve assumed. It is an attestation, meaning an independent licensed CPA firm evaluates your controls and issues a formal opinion under AICPA standards.

The governing framework is SSAE 18, updated through SSAE 21 and AT-C Section 205. No government body issues SOC 2 reports. No badge gets handed over. An auditor looks at your controls, tests them, and tells the world what they found.

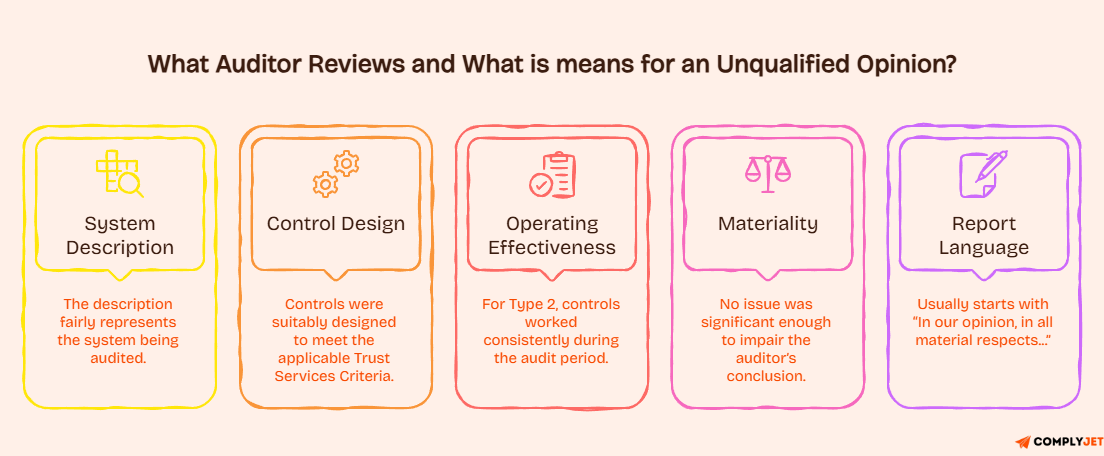

A SOC 2 unqualified opinion means the auditor reviewed your system description, your control design, and for a SOC 2 Type 2 report, the operating effectiveness of your controls over the examination period, and found no material issues with any of them.

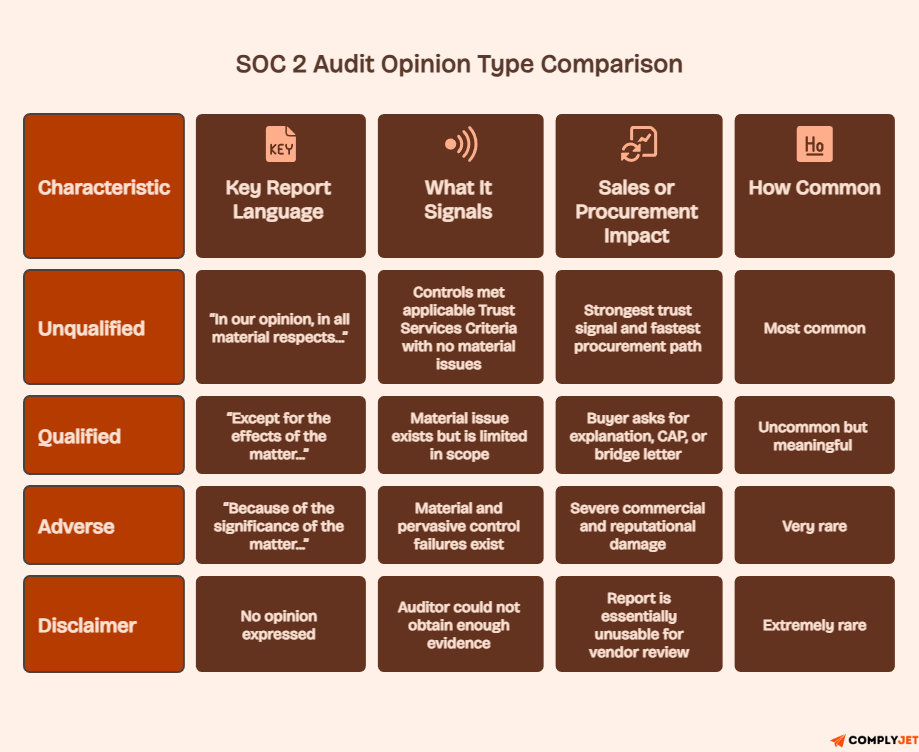

The exact language you will see in the auditor’s report reads: “In our opinion, in all material respects...” That phrase is the signal. It means the auditor is standing fully behind the conclusion.

Read: SOC 2 Type 1 vs Type 2: What’s the difference?

What Does “Unqualified” Mean in an Audit Report?

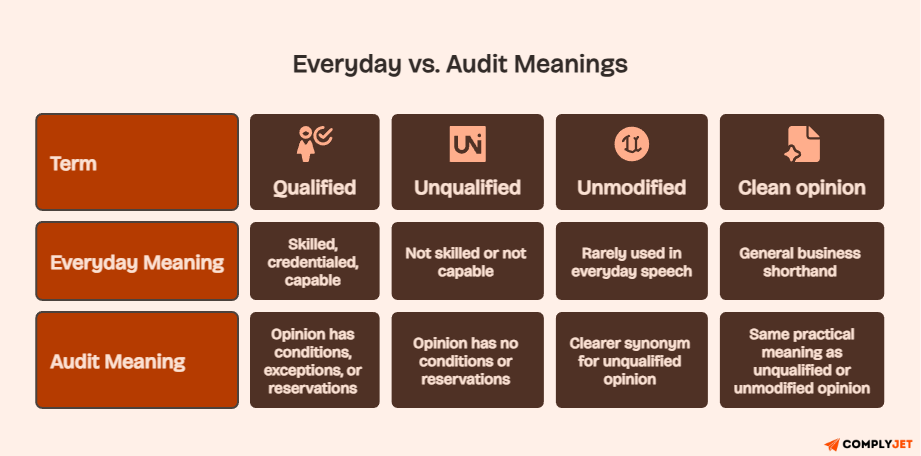

The word “unqualified” modifies the opinion, not the auditor. This is where most people get confused. The auditor is not unqualified. The opinion is unqualified, meaning it carries no limiting qualifications, reservations, or conditions.

The AICPA also uses the term “unmodified opinion” in SSAE 21 as a clearer synonym. Both terms mean the same thing: the auditor’s conclusion stands without restriction. If you see “unqualified” or “unmodified,” you are looking at the outcome every SOC 2 examination should aim for.

Why this matters?

Buyers scan the opinion section before they read anything else in your report. If the auditor’s language starts with “In our opinion, in all material respects,” you are in good shape. If it starts with “except for,” you have a conversation ahead of you.

To be honest, the unqualified opinion is the gold standard of opinions to obtain with an attestation engagement. Enterprise procurement teams treat it as a trust signal too.

It unlocks enterprise RFP eligibility, shortens security questionnaire cycles, and builds investor confidence in ways that a general “we completed a SOC 2 audit” statement simply does not.

Now that you understand what a SOC 2 unqualified opinion means, the next question most founders ask is: why does the best possible outcome have the word “unqualified” in it?

Why Is It Called an “Unqualified” Opinion?

In everyday English, “qualified” means skilled, credentialed, and capable. Something positive. “Unqualified” suggests the opposite. So when founders hear that their goal is to get an “unqualified” opinion, many of them pause.

Audit terminology works differently. In the language of attestation standards, “qualified” describes the opinion itself, not the person giving it.

A qualified opinion is one that comes with qualifications, which in this context means specific conditions, exceptions, or reservations attached to the conclusion. The opinion is “qualified by” those stated exceptions.

An unqualified opinion has none. It stands as a complete, unconditional endorsement.

PCAOB AS 3101 is formally titled “The Auditor's Report on an Audit of Financial Statements When the Auditor Expresses an Unqualified Opinion.” That title alone confirms how foundational this naming convention is in U.S. auditing standards. It is deliberate, and it goes back decades.

The AICPA recognized this creates confusion. SSAE 21, effective June 2022, introduced “unmodified opinion” as the cleaner synonym.

However, both terms are currently valid and used interchangeably across audit firms and compliance platforms. You will see both in reports, vendor communications, and procurement questionnaires.

A simple way to think about it would be an “unqualified endorsement” in everyday language means you love something without reservation. A “qualified endorsement” means you mostly like it, but there is something you need to flag first. Audit opinions work the same way.

Founder’s tip!

When a prospect sends you a security questionnaire asking about your SOC 2 opinion type, do not just write “unqualified.” Add one sentence explaining what it means. Many procurement reviewers are not auditors and will benefit from that context.

This naming confusion is real. A Reddit thread in r/cybersecurity titled “types of opinions for a SOC2 audit (pass/fail)” shows practitioners actively debating whether SOC 2 works like a pass/fail system. It does not. But the confusion is widespread enough that it shows up everywhere.

Now you know the answer, and more importantly, you understand why. So, now we get to discuss the rest of the opinion types that exist.

What Are the 4 SOC 2 Audit Opinion Types?

Not all SOC 2 reports carry the same outcome. Under AICPA attestation standards, there are four distinct opinion types a service auditor can issue.

Two are rare enough that many auditors have never personally issued one. Knowing all four is important whether you are the organisation being audited or a buyer evaluating a vendor’s report.

Unqualified Opinion: The Clean Bill of Health

An unqualified opinion is the auditor’s full endorsement. It means your system description was fairly presented, your controls were appropriately designed to meet the applicable Trust Services Criteria, and, for a Type 2 report, they operated effectively throughout the examination period.

One nuance that surprises many founders is that an unqualified opinion does not mean zero exceptions were found. It means no individual or collective exceptions rose to a level of materiality that prevented your organisation from meeting the applicable criteria. You can have documented findings in Section IV of your report and still receive a clean opinion.

Qualified Opinion: What it Means in a SOC 2 Report

A qualified SOC 2 opinion contains the phrase “except for” in the auditor’s opinion paragraph. That phrase is the fingerprint. It means the auditor found issues that are material but not pervasive, meaning significant enough to flag, but limited to specific areas rather than spread across your entire control environment.

The qualified opinion is accompanied by a dedicated section called the Basis for Qualified Opinion. This paragraph identifies exactly which Trust Services Criteria failed and why. More on that section in detail shortly.

Adverse Opinion vs. Qualified: How They Differ

Both qualified and adverse opinions involve material issues. The line between them is pervasiveness. A qualified opinion is material but confined. An adverse opinion is both material and pervasive, meaning the failures are widespread enough that the organization’s entire system cannot be relied upon.

PCAOB AS 3105 governs the distinction. The report language for an adverse opinion reads: “because of the significance of the matter referred to in the preceding paragraph...” That framing signals a fundamental breakdown in the control environment, not an isolated gap.

Note!

Adverse opinions are so rare that audit firms have rarely or never issued one. The collaborative nature of SOC 2 audits, where auditors flag issues in real time, keeps most examinations well clear of this outcome.

Disclaimer of Opinion: When No Opinion Is Possible

A disclaimer of opinion is not triggered by poor controls. It happens when the auditor cannot obtain sufficient evidence to form any conclusion at all. Common causes include management restricting access to documentation, key records being unavailable, or an organization entering the audit with no prior preparation and failing to provide basic evidence.

The critical distinction from adverse: an adverse opinion means the auditor gathered enough evidence to conclude that pervasive failures exist.

A disclaimer means the auditor simply could not gather enough evidence to conclude anything. As Wolf and Company notes, disclaimers and adverse opinions are both “very rare” in practice, and a disclaimer essentially renders the report unusable for any vendor evaluation purpose.

What Does a SOC 2 Qualified Opinion Mean for Your Business?

Receiving a qualified SOC 2 opinion does not mean your company is insecure. It does not mean all your controls failed. It means the auditor identified issues that were material enough to affect a specific Trust Services Criterion, and those issues were limited in scope rather than pervasive.

Under AICPA SSAE 18 (AT-C Section 205), two conditions can trigger a qualified opinion.

The first is a material misstatement or control deficiency that is confined to a specific area.

The second is a scope limitation, where the auditor could not obtain sufficient evidence for specific controls and believes the possible effects would be material but not pervasive.

Either way, the auditor includes the phrase “In our opinion, except for the effects of the matter(s) described in the Basis for Qualified Opinion section...” in the report.

How to Read the Basis for Qualified Opinion Section?

This paragraph appears immediately before the opinion paragraph in the auditor’s report. It is the most important section to read if you receive a qualified opinion, and if you are a buyer evaluating a vendor.

Under AICPA standards, it must include: which Trust Services Criterion failed (for example, CC6.8 -- Logical and Physical Access Controls), what the control was supposed to do as stated in management’s system description, what the control actually did or failed to do, and quantitative context where available.

Here is what a real Basis for Qualified Opinion paragraph looks like:

“Regarding criterion CC6.8: Management's description states that access to [System X] is removed within one business day of employee termination. Testing of this control revealed that in 5 of 25 instances examined, access was not removed within the required timeframe. The longest observed instance was 9 business days after the termination date.”

The “except for” language in the opinion paragraph that follows directly references this section by name. If you are a buyer, this paragraph tells you exactly what failed, how severely, and how often. If you are the vendor, this is the section your customers will read first after seeing the opinion type.

Did you know?

You can quickly identify a SOC 2 report’s opinion type by searching for the word “Opinion” in any SOC 2 PDF. If the first sentence after that heading starts with “In our opinion, in all material respects,” you have an unqualified opinion. If it starts with “except for,” it is qualified.

Testing Exceptions vs. a Qualified Opinion: Not the Same

This is one of the most misunderstood distinctions in SOC 2. Most founders assume that any exception documented in the report means a qualified opinion. That is not how it works.

Exceptions, also called findings, are factual records of individual control failures noted during testing. An example: a control requires security training within 30 days of hire, and one employee completed it on day 35. That is an exception. It gets documented in Section IV of the report.

A qualified opinion is the auditor’s professional judgment that the impact of one or more exceptions is material enough to impair the organisation’s achievement of a specific Trust Services Criterion.

Most SOC 2 Type 2 reports contain some exceptions. Most still carry unqualified opinions. The auditor evaluates severity, pervasiveness, and whether compensating controls mitigate the impact before elevating any finding to a qualified opinion.

Understanding what causes that escalation is where the real value lies, and that is exactly what the next section covers.

What Causes a Qualified SOC 2 Opinion?

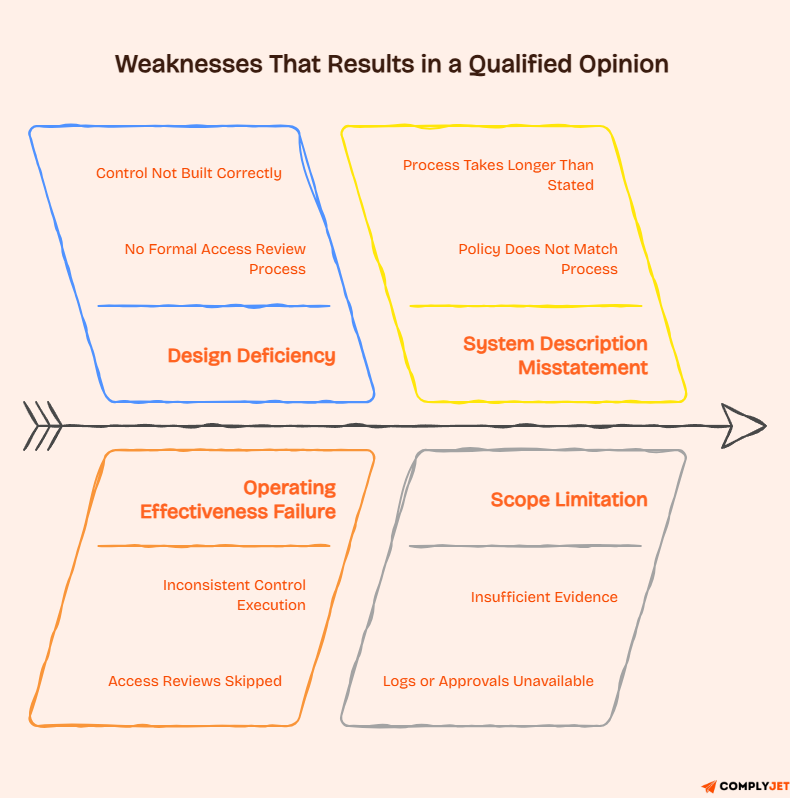

Qualified opinions do not appear randomly. They trace back to one of four root causes, and understanding which category triggered yours determines how you fix it and how fast you can get back to an unqualified audit result.

The four root causes are:

- Design deficiency, where the control was never built correctly in the first place

- Operating effectiveness failure, where the control exists but was not consistently followed during the audit period

- System description misstatement, where the written description in the report does not match what the organization actually does

- Scope limitation, where the auditor could not obtain sufficient evidence for specific controls.

The three most common Trust Services Criteria-level triggers for qualified opinions are:

- CC6.8 (terminated employee access removal): Policy requires access removal within a specific number of business days after termination, and testing reveals delays. According to SOC 2 auditors, this is the single most-reported exception category in SOC 2 Type 2 audits.

- CC6.3 (periodic access reviews): Reviews not conducted on schedule, incomplete documentation, or reviews that did not cover the required scope.

- CC8.1 (change management): Missing authorisation documentation, deployments pushed without required approvals, or changes that lack evidence of pre-deployment testing.

If your SOC 2 gap analysis reveals weaknesses in any of these three areas, address them before your audit period begins.

Design Deficiency vs. Operating Effectiveness Failure

These two categories look similar on the surface, but require completely different remediation approaches.

A design deficiency means the control was not built correctly. There may be no access review process at all, or the process lacks defined ownership and a documented scope. The control simply does not exist in a form that could meet the criterion. No amount of “trying harder” fixes a design deficiency. You have to rebuild the control from scratch.

An operating effectiveness failure means the control exists and is well-designed, but it did not function consistently during the audit period. Access reviews were scheduled but skipped twice. Change approvals were required but not documented for three deployments. The structure is sound. The execution broke down.

Tip!

An operating effectiveness failure is typically easier to remediate than a design deficiency. Automation is usually the fastest path. Manually tracking terminated employee access removal in a spreadsheet will fail eventually. Connecting your HR system to your identity provider removes the human dependency entirely.

The distinction matters because auditors, buyers, and your own remediation team will treat them differently. A design deficiency suggests systemic immaturity. An operating effectiveness failure suggests a fixable process gap.

How Common Are Qualified Opinions in SOC 2 Reports?

The AICPA does not publish centralised statistics on qualified opinion frequency. There is no public database tracking how many SOC 2 reports each year carry each opinion type.

That gap often leads founders to assume qualified opinions are either extremely rare or extremely common. The truth is somewhere in between.

Unqualified opinions are the standard outcome for well-prepared organisations. But qualified opinions are described as “not uncommon” and occurring with “meaningful frequency,” particularly in first-year audits.

The sheer volume of audit firm content covering qualified opinions is itself a signal that these outcomes occur regularly enough to warrant attention.

The organisations most likely to receive a qualified opinion share recognisable traits.

They are in their first SOC 2 audit without a prior readiness assessment. They experienced rapid growth or significant operational changes during the audit period. They rely on manual compliance processes, which introduce human error in access reviews, training tracking, and change approvals. Any of these conditions alone increases risk. Two or more of them together make a qualified opinion meaningfully likely.

Adverse and disclaimer opinions remain genuinely rare. Career auditors at major CPA firms consistently report never having issued one.

The collaborative audit model that the AICPA promotes, where auditors flag emerging issues in real time under a “no surprises” approach, typically prevents examinations from escalating beyond a qualified opinion.

By the time a formal report is issued, both parties have usually had the opportunity to address any issues that could produce the most severe outcomes.

SOC 2 Qualified vs. Unqualified: What It Means for Vendor Risk

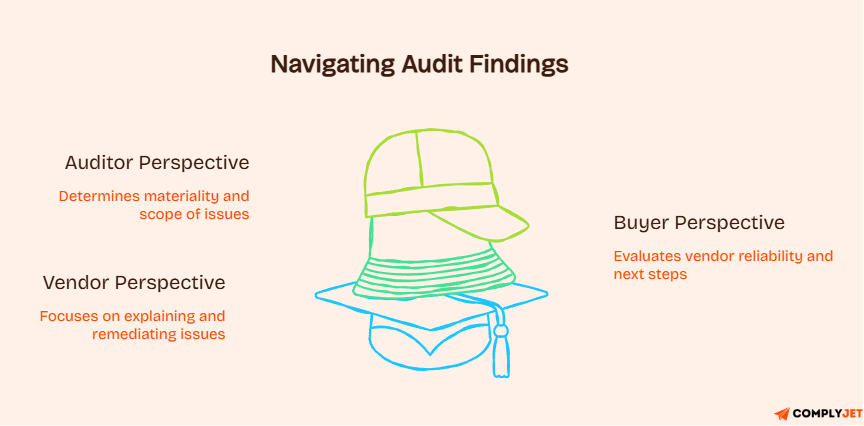

Most content on SOC 2 opinion types is written for the vendor trying to understand their report. But a large portion of people searching this topic are on the other side of the table. They are procurement managers, security analysts, and vendor risk teams who just received a vendor’s SOC 2 report and found a qualified opinion inside. This section is for both.

If you are the vendor, understanding how buyers evaluate a qualified opinion helps you frame your management response, prepare your customer communications, and prioritise remediation.

If you are the buyer, you need a structured process for evaluating risk rather than defaulting to automatic disqualification. As the SANS Institute notes in its expert guide to reviewing SOC 2 reports, a qualified opinion does not automatically disqualify a vendor.

What matters is the severity of the identified issues and the quality of the management response.

How to Evaluate a Vendor’s Qualified SOC 2 Report?

When you receive a vendor’s SOC 2 report and find a qualified opinion, here is the framework to apply before making a risk decision.

- Start with the Basis for Qualified Opinion section.

- Identify which Trust Services Criterion failed, what the control was supposed to do, and what it actually did.

- Evaluate the management response in Section V of the SOC 2 report. A strong management response names the root cause, names the accountable owner, specifies a remediation timeline with measurable milestones, and describes how the control will operate going forward. A weak management response says, “We take security seriously and are working to improve.” The quality of that response tells you as much about the organisation’s maturity as the qualified opinion itself.

- Ask the vendor directly for a bridge letter or Corrective Action Plan (CAP). A SOC 2 bridge letter is a management-attested document stating that the issues identified in the report have since been remediated. It provides interim assurance between the qualified report and the next full audit cycle.

- Request a timeline for the next examination as part of that conversation.

- Document your risk acceptance decision for your own audit trail. Whether you accept, escalate, or decline the vendor, your compliance audit trail should reflect that you evaluated the report, understood the specific finding, and made a reasoned decision.

Risk-Tiering by Trust Services Criteria Category

Not all qualified opinions carry the same weight. The Trust Services Criterion that failed matters significantly. Here is a simple risk-tiering framework:

A qualified opinion in the Security (Common Criteria) category is the most universally serious because Security is the only mandatory Trust Services Criterion. Every SOC 2 report includes it. A qualification here affects the foundational layer of the entire control environment.

A qualification in Availability may be entirely irrelevant if you use that vendor for document storage, but it would be highly material if they host your production environment. Context drives the risk tier, not the category alone.

Why this matters?

Procurement teams that apply blanket disqualification rules to qualified opinions sometimes exclude vendors with minor, remediated findings in optional criteria while accepting vendors with no SOC 2 at all. A structured TSC-tiering approach produces better risk decisions.

The vendor side of this equation is equally important. Once you receive a qualified opinion, the remediation clock starts, and your response in the next few weeks will define how buyers perceive your security program maturity.

What to Do After Receiving a Qualified SOC 2 Opinion?

Receiving a qualified SOC 2 opinion is not the end of the road. Every audit firm that publishes guidance on this topic agrees: a qualified opinion is a meaningful signal, not a verdict. You cannot 'fail' a SOC 2 audit.

The outcome is either unqualified or qualified, both valid for business purposes. What matters is what you do next.

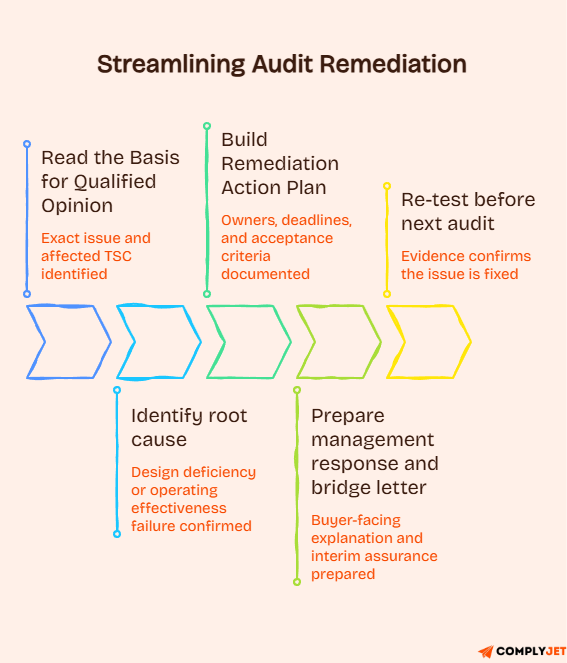

The first step is understanding exactly what triggered the qualification.

Go back to the Basis for Qualified Opinion section and read it as a root cause document. Is the failure a design deficiency or an operating effectiveness failure? The remediation path, timeline, and cost are completely different depending on the answer.

Building Your Remediation Action Plan

A strong Remediation Action Plan (RAP) has three components. Root cause identification, specific action items, and measurable acceptance criteria.

On root cause: design deficiencies require structural rebuilds. If your access review process never had a defined owner or documented scope, you are not going to patch that with a reminder email. You need a new process, proper ownership, and evidence capture built in from day one.

For operating effectiveness failures, the fix is usually automation. Manual processes fail under scale and speed.

If CC6.8 triggered your qualification because terminated employee access was not removed on time, the sustainable fix is connecting your HR offboarding workflow to your identity provider so the removal happens automatically, not because someone remembered to check a list.

The management response you write in Section V of the SOC 2 report is your first public statement about how you are handling this. Make it specific.

An example of a strong management response: “Access removal for terminated employees will be automated through integration between [HR system] and [identity provider], completing within four hours of termination. The IT Security Manager is accountable. The integration will be live by [specific date].”

That level of specificity signals maturity. A vague response signals the opposite.

How to Use a Bridge Letter After a Qualified Opinion?

A bridge letter is a document that management provides to buyers to confirm that the issues identified in a qualified SOC 2 report have since been remediated. It covers the period between when the report ended and the present date.

Bridge letters are not a substitute for a clean re-audit. They are the interim tool that keeps enterprise deals moving while the next examination cycle is underway. In 2025 and 2026, enterprise procurement teams are increasingly requiring them as part of vendor contract requirements. If a buyer asks for one and you cannot provide it, that absence itself becomes a concern.

Alongside the bridge letter, proactive customer communication matters. One page explaining the finding, its scope, and your remediation timeline, sent before a customer asks, is almost always received better than the same information delivered reactively. Buyers want to see that you found the issue, owned it, and fixed it. That narrative is available to you even after a qualified opinion.

Tip!

Schedule your next SOC 2 readiness assessment three to four months before the next audit period begins. Do not wait for the auditor to find remaining gaps. Find them yourself first.

How to Achieve a SOC 2 Unqualified Opinion in 2026?

Achieving a SOC 2 unqualified opinion is not about luck. It is about preparation, consistency, and closing the gaps before the auditor’s testing window opens.

Start with a readiness assessment three to four months before your audit begins. The purpose is to identify control gaps before the auditor does. Any exception your team finds during a readiness review is an exception you can fix. Any exception the auditor finds becomes a documented finding.

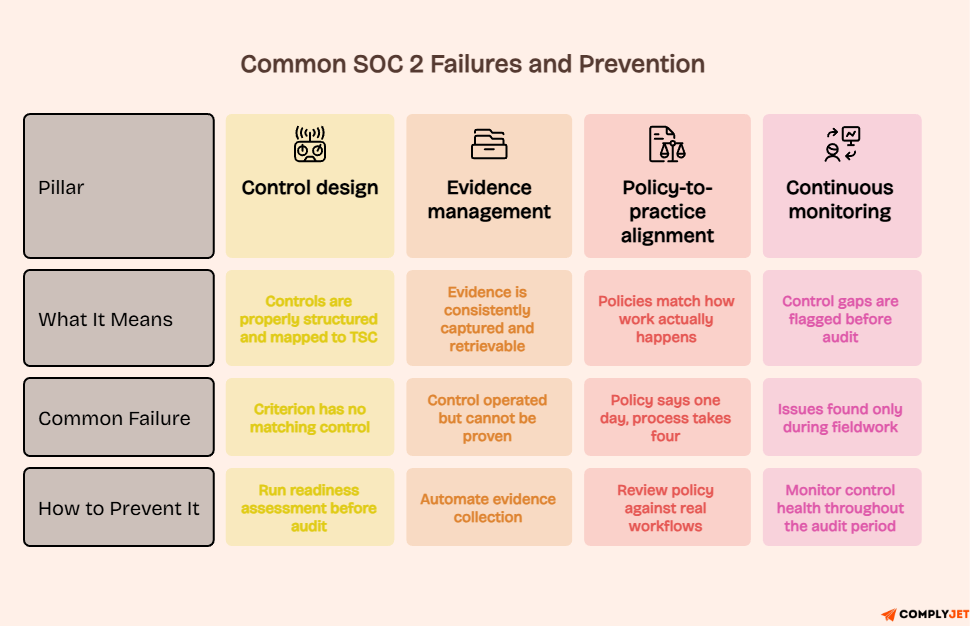

Three pillars determine your outcome.

The first is control design. Every applicable Trust Services Criterion must have a corresponding, properly designed control with a named owner and a documented process. If a criterion has no matching control, an auditor has nothing to test and will note the gap.

The second pillar is evidence management. Evidence of control operation must be captured consistently and retrievably for every testable period during the audit window. A control that operated well but was never documented is functionally invisible to an auditor.

Learn more about what auditors look for in the SOC 2 evidence requirements section of our resources.

The third pillar is policy-to-practice alignment. Written policies must match operational reality. The most common description gap that triggers qualifications is a policy that says one thing and a process that does another.

If your policy states access is removed within one business day and your actual average is four business days, the policy is the problem as much as the process.

In 2026, the organisations achieving unqualified opinions most efficiently are the ones using automated compliance monitoring.

Automation removes the human error that drives the majority of qualification triggers. When access removal is automated, when training completion is tracked in real time, and when change approvals generate their own evidence, the exception rate drops and so does your qualification risk.

One final principle!

Work with an audit firm that flags issues during the examination, not after. The AICPA’s collaborative audit model means auditors should be surfacing emerging concerns in real time.

If a qualified opinion is the first time you heard about a problem, the relationship with your auditor needs recalibration before the next cycle.

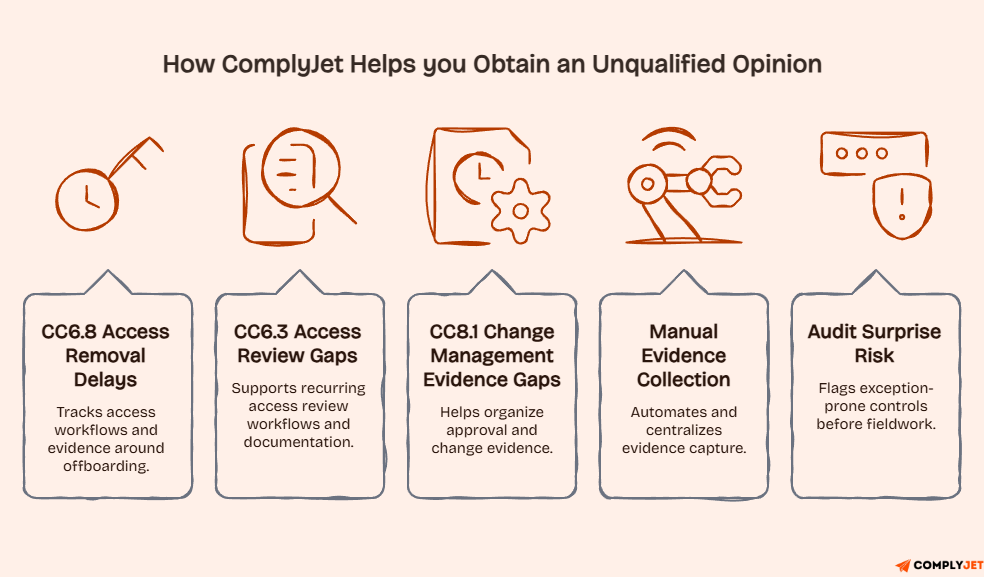

How ComplyJet Helps You Achieve an Unqualified Opinion?

ComplyJet is built for lean SaaS and startup teams that need to reach SOC 2 compliance without building an entire compliance department.

The platform tracks control health in real time, automates evidence collection, and flags exception-prone controls before the audit period ends, which means your team sees the gaps before the auditor does.

Every issue that triggers a qualified opinion, from CC6.8 access removal delays to inconsistent access review documentation, has a corresponding workflow in ComplyJet. The platform does not just tell you what the SOC 2 requirements are. It tracks whether your controls are meeting them right now, in the current period, so there are no surprises when the audit fieldwork begins.

Explore the SOC 2 compliance solution to see how the platform maps to the specific controls and criteria that avoids a qualified opinion risk.

FAQs: SOC 2 Unqualified vs. Qualified Opinion

What does an unqualified opinion mean in a SOC 2 Type 2 report?

In a SOC 2 Type 2 report, an unqualified opinion means the independent service auditor examined your controls over a defined period, typically 6 to 12 months, and found those controls were both suitably designed and operated effectively throughout the entire examination window.

This is a higher evidentiary standard than a Type 1 report, which only addresses the suitability of design at a single point in time. A SOC 2 unqualified opinion is the outcome enterprise buyers expect and is the strongest commercially viable signal of control maturity.

Are qualified SOC 2 opinions uncommon in practice?

Qualified SOC 2 opinions are uncommon relative to unqualified opinions, but they occur with meaningful frequency, particularly in first-year audits and organisations without automated compliance monitoring.

Well-prepared organisations with continuous control and evidence collection rarely receive them. Adverse and disclaimer opinions are genuinely uncommon. Multiple career SOC 2 auditors across major CPA firms report never having issued one.

What does AICPA guidance say about the meaning of a SOC 2 qualified opinion?

Under AICPA SSAE 18 (AT-C Section 205), a service auditor issues a qualified opinion when the subject matter contains a material misstatement or the engagement is limited in scope, and the auditor concludes the effects are material but not pervasive.

The 2022 SSAE 21 update reinforced this definition and introduced “modified opinion” as the umbrella term covering qualified, adverse, and disclaimer outcomes. AICPA guidance requires the auditor to disclose the basis for qualification in a dedicated paragraph immediately before the opinion paragraph.

What does “material but not pervasive” mean in a SOC 2 qualified opinion?

“Material but not pervasive” is the precise threshold that separates a qualified opinion from an adverse opinion. “Material” means the issue is significant enough to affect a reasonable user’s reliance on the report.

“Not pervasive” means the issue is confined to specific, named areas rather than being widespread throughout the entire control environment. When issues are both material and pervasive, the auditor issues an adverse opinion instead.

What is the difference between a SOC 2 qualified opinion and an adverse opinion?

A qualified opinion means the auditor found material issues limited to specific areas of the control environment. An adverse opinion means the issues are both material and pervasive, so widespread that stakeholders cannot rely on the organisation’s system as a whole. In practical terms, a qualified opinion might affect one Trust Services Criterion while the rest of the report remains reliable.

An adverse opinion renders the entire system description unreliable. Adverse opinions are extremely rare in SOC 2 practice.

How does a SOC 2 qualified opinion compare to a disclaimer of opinion in severity?

A disclaimer of opinion is not necessarily more severe than a qualified opinion; it is categorically different. A qualified opinion means the auditor gathered evidence, found material issues in limited areas, and issued a restricted endorsement.

A disclaimer means the auditor could not gather sufficient evidence to form any opinion at all. Both are undesirable, but a qualified opinion at least provides usable information. A disclaimer leaves the entire report without auditor endorsement and is essentially unusable for vendor evaluation purposes.

What does a SOC 2 unqualified opinion mean for a SaaS company specifically?

For a SaaS company, a SOC 2 unqualified opinion is both a compliance milestone and a commercial asset. It signals to enterprise buyers that your security controls met the applicable Trust Services Criteria throughout the audit period without material exceptions.

This accelerates procurement decisions, unlocks enterprise RFP eligibility, and reduces security questionnaire burden. Many SaaS companies issue formal press releases upon receiving their first unqualified opinion because of its direct impact on enterprise sales cycles.

Can software help track readiness for a SOC 2 unqualified opinion?

Yes. Compliance automation platforms are built to track SOC 2 control readiness in real time, automate evidence collection, flag exceptions before the audit period ends, and manage access review workflows. These are the leading triggers of qualified opinions when handled manually.

ComplyJet monitors control health continuously, giving your team the visibility to remediate exception-prone controls before the auditor documents them. You can also review SOC 2 compliance software options to understand what features matter most.

What are the SOC 2 qualified opinion’s implications for vendor risk programs?

For vendor risk programs, a supplier’s qualified SOC 2 opinion triggers structured additional due diligence rather than automatic disqualification. The first step is reading the Basis for Qualified Opinion paragraph to identify which Trust Services Criterion failed and whether the failure is relevant to your specific use case.

A Security (Common Criteria) failure is universally material. Failures in optional criteria, such as Availability or Privacy, may carry different risk levels depending on how the vendor’s service is used. Procurement teams should also evaluate the quality of the management response and whether a bridge letter or CAP has been provided.

Conclusion

That $95,000 deal we discussed earlier fell apart because two words in the auditor’s opinion section told the procurement team what was true about the vendor’s controls during that audit period.

Those words are the direct result of how controls were designed, monitored, and evidenced throughout the year.

A SOC 2 unqualified opinion is the outcome of a control environment that leaves an auditor no alternative conclusion.

At the same time, a SOC 2 qualified opinion is not the end of the road. It is specific feedback that, when acted on quickly and transparently, can be remediated before your next cycle and communicated to buyers in a way that demonstrates security program maturity rather than hiding it.

In 2026, when enterprise buyers check the opinion section before they read anything else, there is no stronger signal than “in our opinion, in all material respects.”

Ready to build the control environment that earns that conclusion? Book a Demo