Picture two teams at a fintech company that just announced its IPO.

Team Finance is deep in SOX readiness, building evidence packs for their external auditors. Team Engineering just lost a $400,000 enterprise deal because the prospect asked for a SOC 2 Type 2 report, and the sales team did not have one.

Both teams are stressed. Both are doing compliance. And then, in a Thursday conference room, someone asks: "Can we just give the SOX auditors our SOC 2 report as evidence?" The room goes quiet. Nobody is sure.

That question is costing real companies real money in 2026. The SOC 2 vs SOX confusion is not a minor misunderstanding. It sends teams submitting wrong evidence to the wrong auditor, wasting six months earning a report their investor relations team never asked for, and losing enterprise deals because they handed a customer the wrong document entirely.

This guide answers that conference room question completely. You will get the full comparison, the cost data nobody shares, the controls overlap map, and the seven mistakes teams keep repeating this year.

Start your SOC 2 compliance journey with ComplyJet before your next enterprise renewal cycle.

If you need the core differences before diving into detail, this is what you need to know.

SOC 2 vs SOX at a Glance

- SOX is a US federal law (Public Law 107-204, signed July 30, 2002). SOC 2 is a voluntary AICPA attestation framework. No government enforces SOC 2.

- SOX protects investors by ensuring the accuracy of public company financial statements. SOC 2 proves to enterprise buyers that a service provider's systems are secure and reliable.

- SOX is mandatory for every SEC-listed public company. SOC 2 is voluntary, but 77% of enterprises now require it from vendors as their top procurement requirement (ISC2, 2025).

- SOX is enforced by the SEC and the PCAOB. SOC 2 is governed by the AICPA. SOX Section 404(b) auditors must be PCAOB-registered. SOC 2 auditors must be licensed CPA firms.

- SOC 2 covers five Trust Services Criteria: Security (mandatory), Availability, Processing Integrity, Confidentiality, and Privacy. SOX covers four IT General Control categories: Access Controls, Change Management, Computer Operations, and Program Development.

- SOC 1, not SOC 2, is more directly related to SOX. Public companies request SOC 1 Type 2 reports from vendors during SOX 404 ITGC testing, not SOC 2 reports.

- SOC 2 is not a certification. It produces an attestation report from a licensed CPA. There is no AICPA-issued certificate and no pass or fail outcome.

- SOX non-compliance carries criminal penalties. CEOs and CFOs who willfully certify false reports face up to $5 million in fines and 20 years imprisonment (Section 906). SOC 2 non-compliance has zero legal penalties.

What Is SOX? The Law Born From Corporate Scandal

SOX did not come from a policy paper or a think tank. It came from two of the biggest corporate accounting frauds in US history, and Congress passed it with near-unanimous votes because the alternative was worse.

Understanding SOX means understanding what it was built to prevent. Once you see that, every section, every control category, and every penalty makes complete sense.

What Does SOX Stand For?

SOX stands for the Sarbanes-Oxley Act of 2002, formally Public Law 107-204. It was named after Senator Paul Sarbanes of Maryland and Representative Michael Oxley of Ohio. It was signed into law on July 30, 2002, by President George W. Bush.

The trigger was Enron, which filed for bankruptcy in December 2001 after concealing billions in debt. Its auditor, Arthur Andersen, was implicated in the cover-up. Then WorldCom revealed it had overstated earnings by more than $3.8 billion over five quarters, ultimately reaching a $70 billion total restatement. It became the largest US bankruptcy at the time.

Congress responded fast. The Senate voted 97 to 0. The House voted 423 to 3. SOX uses the COSO Internal Control Framework to organise its requirements across five components: Control Environment, Risk Assessment, Control Activities, Information and Communication, and Monitoring Activities.

Tip!

SOX was not designed for tech companies or SaaS vendors. It was designed for public companies with SEC-registered securities. If that is not your company, SOX likely does not apply to you directly.

SOX Section 302 vs 404: What Executives Must Sign Off On?

Section 302 and Section 404 are the two sections that compliance teams spend the most time on. They are distinct obligations, not the same thing.

Section 302 requires CEOs and CFOs to personally certify every quarterly 10-Q and annual 10-K filing with the SEC. They must affirm that there are no material omissions, that financial statements fairly represent the company's condition, and that they assessed disclosure controls within 90 days prior to filing. This is a quarterly obligation.

Section 404 is the annual internal control assessment.

Section 404(a) requires management to assess the effectiveness of Internal Controls over Financial Reporting (ICFR) each year.

Section 404(b) requires an external auditor registered with the PCAOB to attest to that assessment. Section 404(b) applies to large accelerated filers (public float above $700 million) and accelerated filers (float between $75 million and $700 million).

Non-accelerated filers and Emerging Growth Companies are exempt from 404(b). The Section 404 integrated audit is governed by PCAOB Auditing Standard AS 2201.

Section 802 requires audit workpapers and related records to be retained for 7 years. Knowingly destroying records relevant to a federal investigation carries up to 20 years imprisonment.

Section 906 sets criminal penalties: willfully certifying a false report means up to $5 million in fines and 20 years in prison. Knowingly certifying a false report is up to $1 million and 10 years. Corporate criminal fines reach up to $25 million per offense.

The 4 SOX IT Controls Every ITGC Team Must Know

SOX IT General Controls (ITGCs) exist for one reason: failures in IT can affect the accuracy of financial statements. Every ITGC category traces back to that risk.

The four ITGC categories are:

- Access Controls: who can access financial systems; user provisioning and deprovisioning; least-privilege enforcement; multi-factor authentication; periodic access reviews; segregation of access roles

- Change Management: structured approval, testing, and documentation before changes go live in financially significant systems; separation of development and production environments

- Computer Operations: system monitoring, backup and recovery, job scheduling, incident management, and data centre physical security

- Program Development: SDLC governance for new system implementations and significant software development projects

Did you know?

A single weak access control in a financial system is not just a security issue under SOX. It is a potential material weakness in ICFR, which must be disclosed publicly in your annual 10-K.

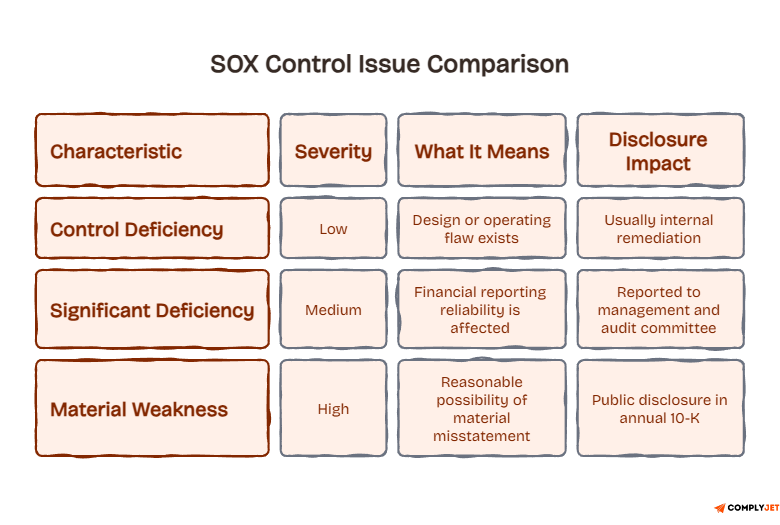

Material Weakness vs Significant Deficiency: The Stakes

SOX uses a three-tier severity scale to classify control failures. Understanding where a deficiency falls on this scale determines whether you disclose it publicly.

A control deficiency is the lowest level. It is a design or operational flaw where management or employees cannot prevent or detect misstatements on a timely basis.

A significant deficiency is the middle level. It adversely affects the company's ability to initiate, authorise, record, process, or report financial data. It carries more than a remote likelihood of a more-than-inconsequential misstatement slipping through.

A material weakness is the highest level. It means there is a reasonable possibility that a material misstatement of annual or interim financial statements will not be prevented or detected. Material weaknesses must be publicly disclosed in the annual 10-K. That disclosure is public record and can affect your stock price.

Research from Harvard Law found that companies without material weaknesses experienced a 10% share price premium above the Russell 3000 index, and borrowing costs declined 50 to 150 basis points for companies that improved their internal controls.

Now that you have the full SOX picture, it is time to look at the other side of the comparison, and where it fundamentally breaks from the legal world SOX inhabits.

What You Need to Know About SOC 2?

SOC 2 lives in a completely different world from SOX. No government created it. No government enforces it. It exists because enterprise buyers needed a way to evaluate the security of the vendors they bring into their data supply chain.

The most important thing to understand about SOC 2 is what it is not.

Getting this wrong has real consequences in sales conversations and procurement reviews.

SOC 2 stands for System and Organisation Controls 2. The name was updated from Service Organisation Controls by the AICPA, which governs the framework. The underlying attestation standard is SSAE 18 (Statement on Standards for Attestation Engagements No. 18), specifically AT-C Sections 105 and 205. SSAE 18 replaced SSAE 16 in May 2017.

SOC 2 replaced SAS 70, which was introduced in the 1970s and only addressed financial reporting controls. As companies moved operations to cloud vendors, SAS 70 had no way to assess security or operational reliability. The AICPA introduced SOC 2 in 2010 to fill that gap.

Here is the myth that trips up sales teams across the industry.

SOC 2 Is Not a Certification

There is no such thing as being SOC 2 certified. The AICPA does not issue certificates. SOC 2 produces an attestation report, which is a licensed CPA's professional opinion on the state of your controls. There is no pass or fail. The report documents your controls and any exceptions the auditor found during the audit period.

Compare that to ISO 27001, which is a true certification issued by an accredited certification body, with a certificate and an expiry date. Only licensed CPA firms can issue SOC 2 reports under AT-C Section 205. IT consultancies and security vendors cannot.

SOC 2 is also a restricted-use document. It is shared only under NDA with current customers, prospects, and business partners. SOC 3 is the public-facing summary of a SOC 2 examination but without the control detail, testing procedures, or exceptions. It can be freely posted on your website.

Why this matters?

When your sales team says "we are SOC 2 certified," a sophisticated enterprise security reviewer will notice. The correct phrase is "we have a SOC 2 Type 2 attestation report." That one word signals you actually understand the framework.

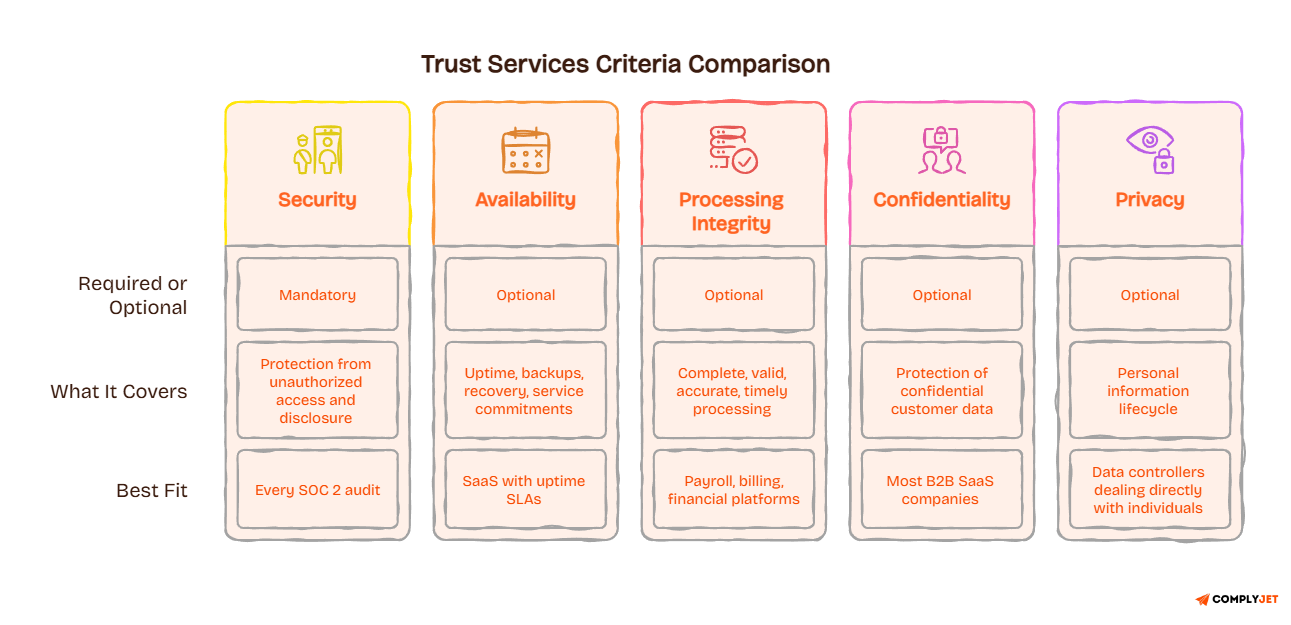

The 5 Trust Services Criteria: What Each One Covers

SOC 2 audits are organised around five Trust Services Criteria (TSC). You do not have to include all five. You select the ones relevant to your commitments to customers.

- Security (CC1-CC9): The only mandatory TSC. Every SOC 2 engagement must include it. Nine Common Criteria govern protection from unauthorised access, disclosure, and damage. This is the baseline.

- Availability (A1): Optional. Covers system uptime and SLA commitments. Include it if you have committed to specific uptime guarantees to customers.

- Processing Integrity (PI1): Optional. Covers whether your system processing is complete, valid, accurate, timely, and authorised. Best for payroll processors and financial platforms.

- Confidentiality (C1): Optional. Covers the protection of information designated confidential in your contracts. The right choice for most B2B SaaS companies that handle customer PII as a data processor.

- Privacy (P1-P8): Optional. Covers the full personal information lifecycle from collection to disposal. This is for data controllers who interact directly with individuals, not data processors. It is the most complex and resource-intensive TSC category.

According to the CBIZ 2024 SOC Benchmark Study, Security appears in 100% of SOC 2 reports. Availability is in 75.3%. Confidentiality jumped dramatically from 34% to 64.4% in a single year. That jump reflects how many enterprise contracts now explicitly require confidentiality commitments from vendors.

SOC 2 Type 1 vs Type 2: Which Report Do Buyers Want?

The Type 1 versus Type 2 distinction is where many early-stage companies get their strategy wrong. Both are valid reports. They answer different questions.

A SOC 2 Type 1 is a point-in-time snapshot. It assesses whether your controls are designed correctly as of a specific date. Timeline: 3 to 6 months total. Cost: $7,500 to $60,000. It is useful for an early win or to unblock a sales cycle with a less demanding buyer.

A SOC 2 Type 2 covers a defined audit period, most commonly 6 to 12 months. It assesses whether your controls were designed correctly AND operated effectively throughout that period. Timeline: 6 to 15 months. Cost: $12,000 to $100,000 or more. Enterprise procurement teams almost always require a Type 2. A Type 2 report older than 12 months is commonly rejected. SOX 404 has no Type 1 equivalent. It is always a period-based annual assessment.

The cost gap between frameworks is significant, and most comparison articles skip the real numbers entirely. That deserves its own section, which is coming. First, there is a nuance in the SOC 1 versus SOC 2 versus SOX relationship that changes how you handle vendor evidence requests.

SOC 2 vs SOX: The Full Comparison

SOC 2 and SOX answer to completely different masters. Here is every meaningful comparison dimension in one place.

SOX is a legal obligation to capital markets. SOC 2 is a commercial obligation to customers. They serve different audiences, live under different rules, and cannot substitute for each other.

SOC 1 vs SOC 2 vs SOX: The Nuance No One Explains

This is the section that answers the Thursday conference room question. Most people debating SOC 2 vs SOX do not realise there is a third actor in this story: SOC 1. And SOC 1 is the one that actually connects to SOX most directly.

Getting this distinction right is what separates teams that handle compliance audits cleanly from teams that spend weeks resubmitting rejected evidence.

Why SOC 1 Is More Related to SOX Than SOC 2?

SOC 1, governed by SSAE 18 AT-C Section 320, covers controls at service organisations that are relevant to their customers' Internal Controls over Financial Reporting. That is the direct SOX connection.

If you are a payroll processor, a payment processor, an equity management platform, or a billing provider, the controls you maintain can directly affect the accuracy of your customers' financial statements. When a public company does its SOX 404 ITGC testing, its auditors request SOC 1 Type 2 reports from those vendors, not SOC 2 reports. They need ICFR-specific assurance, which SOC 2 does not provide.

SOC 2 covers security and operational controls. A SOC 2 report does not satisfy a SOX auditor's request for ICFR-related vendor assurance. If a customer comes to you asking for evidence to support their SOX compliance program and you hand them your SOC 2 report, you are giving them the wrong document.

Founder's tip!

If your customers are public companies running SOX programs, ask them which report type they need from you before your next renewal. The answer shapes which audit you should be prioritising.

When SOC 2 Evidence Can Support SOX Testing?

SOC 2 and SOX do share control territory in one specific area: IT General Controls. This is where careful scoping creates real efficiency gains.

Access review screenshots, change approval records, incident response logs, and MFA configuration evidence collected for your SOC 2 audit can sometimes be reused as SOX ITGC evidence for the same systems. The potential is real. But there is a hard requirement attached to it.

SOC 2 is scoped to the service system you define at the start of the engagement. SOX ITGC must cover all systems that affect the accuracy of financial statements. Those two scopes may not fully overlap. Evidence collected for systems outside the SOX financial scope cannot be used for SOX testing.

External SOX auditors will reject evidence without formal documented scope alignment. The reuse only works when scope is explicitly mapped and approved before the testing period begins.

SOC 2 and SOX Controls: Where They Overlap and Where They Don't?

The controls overlap between SOC 2 and SOX is real, documented, and valuable when handled correctly. It is also one of the most misunderstood areas in compliance operations, because teams assume the overlap is broader than it actually is.

This section gives you the exact mapping so you know what you can and cannot count on when building a combined evidence strategy.

The 4 SOX ITGC Domains and Their SOC 2 Counterparts

The overlap is highest in access management, change management, and system operations. These three areas are where teams with both SOC 2 and SOX programs can build shared evidence routines that serve both audits simultaneously.

Segregation of Duties: Where Both Frameworks Agree?

Segregation of duties (SoD) is one of the most consistently enforced controls across both frameworks. Under SOX, no single person can authorise and record a financial transaction. Responsibilities for authorising, recording, and handling related assets must be separated.

Under SOC 2, CC5 and CC6 together enforce SoD across system operations. No single person should be able to both develop and deploy changes to production. This is the most consistent alignment point between the two frameworks.

Access review evidence collected for SOC 2 CC6 almost always applies directly to the SOX access control ITGC. If you are running SOC 2 access reviews quarterly or more frequently, that evidence is likely reusable for SOX testing on the same systems. This is where scoping documentation pays the biggest dividend.

What SOC 2 Evidence Can and Cannot Be Reused for SOX?

Evidence that can typically be reused with proper scope documentation:

- Access review logs

- Change approval records and ticket histories

- User provisioning tickets

- Incident response runbooks

- MFA configuration screenshots

Evidence that cannot directly substitute:

- The SOC 2 report itself as ICFR evidence (different purpose and scope)

- Controls scoped to systems outside the SOX financial reporting environment

- Privacy TSC evidence (no SOX analogue exists for it)

The process is straightforward. Work with your SOX auditors before the testing period to formally map and document which systems appear in both your SOC 2 scope and your SOX ITGC scope. Do this once, document it properly, and the evidence reuse is defensible. Skip this step and evidence gets rejected at the worst possible moment.

ComplyJet automates evidence collection and maps shared controls across frameworks. One access review. One change record. One piece of evidence serving both audits. Book a free demo to see how it works.

Who Needs SOC 2 vs SOX?

The SOC 2 vs SOX question has a different answer depending on what stage your company is at. Getting this wrong means spending time and money on the wrong framework entirely.

This decision guide covers every scenario compliance teams ask about most in 2026.

SaaS Companies: Do You Need SOC 2 or SOX?

If you are a private SaaS company, the answer is SOC 2. SOX does not apply to private companies under Section 404. You are not a US-listed public company.

The commercial pressure to get SOC 2 is now significant. 77% of enterprises cite standards compliance (including SOC 2) as their top vendor requirement (ISC2 2025, 1,062 respondents). A SOC 2 report removes a security review process that costs IT decision-makers an average of 6.5 hours per week per vendor being evaluated. That friction is why enterprise deals stall without it.

Start with SOC 2 Type 1 for a fast first win in 3 to 6 months. Then progress to Type 2, which is what enterprise procurement teams actually require for sustained vendor trust. If you want to understand the SOC 2 audit process before committing, that is the right next step.

What Private Companies Need to Know About SOX?

Most private companies have zero SOX obligations under Section 404. But two provisions extend beyond public companies, and they catch teams off guard.

Section 806 whistleblower protections apply to employees of private contractors and subcontractors that serve public companies. The US Supreme Court confirmed this in Lawson v. FMR LLC in 2014. If your company services a public company client and an employee reports wrongdoing related to that client, they have federal whistleblower protection.

Section 802, the document destruction prohibition, also applies broadly to anyone involved in federal investigations. This is not limited to public companies. If your business handles records relevant to a federal financial investigation, Section 802 applies to you.

Note: Private company employees are not protected by Section 806 for reporting purely private-company wrongdoing. The protection activates only when the reported conduct relates to the public company client.

Pre-IPO: When SOX Compliance Kicks In?

SOX compliance obligations activate the moment your registration statement is filed with the SEC, not when you ring the opening bell.

Section 302 certifications are required immediately on IPO. Section 404(a) management assessment is required in your first annual 10-K after going public. Section 404(b) external auditor attestation depends on your filer classification. Emerging Growth Companies (EGCs) are exempt from 404(b) for up to 5 years post-IPO or until revenue reaches $1.235 billion.

Big 4 firms consistently recommend starting SOX readiness at least 24 months before your target IPO date. Companies that wait until IPO year find themselves in a 12-month scramble for controls that should have taken 2 years to build. Common gaps in the private-to-public transition include no formal documentation culture, no audit committee independence, no SDLC governance, and weak change management. Your SOC 2 gap analysis work, if done right, gives you a controls foundation you can extend into the SOX financial system scope.

Public Companies That Also Sell Services Need Both

A US-listed SaaS or cloud company has no choice. It needs both.

SOX proves financial controls to regulators and investors. That is a legal obligation with criminal penalties. SOC 2 proves security controls to customers and prospects. That is a commercial obligation with deal consequences. They serve different audiences and cannot substitute for each other. Controls overlap in shared systems allows some evidence reuse and cost optimization when you handle the scoping correctly.

SOC 2 vs SOX: Real Compliance Costs in 2026

The cost gap between these two frameworks is one of the most practically important differences teams encounter. Most SOC 2 vs SOX comparison articles skip the real numbers. This section does not.

Understanding cost helps you set realistic budgets, make the case to leadership, and avoid being blindsided in the second year.

What SOX Compliance Actually Costs by Company Size?

SOX compliance is an ongoing annual operational expense, not a one-time project. It requires dedicated internal audit resources, external auditor fees, and continuous remediation work.

According to Protiviti's 2024 SOX Compliance Survey and GAO Report GAO-25-107500:

The Fortune 500 average in their first year of SOX compliance (2004) was $5.1 million. When a company becomes non-exempt from Section 404(b), the GAO found a median external audit fee increase of $219,000 (a 13% jump) in the transition year alone. In one documented case, audit testing hours grew from 3,000 in 2012 to 8,000 in 2024, with fees climbing from $900,000 to $3 million.

What SOC 2 Audit Costs in 2026: Type 1 and Type 2

SOC 2 is a very different cost profile. It is primarily treated as a one-time investment with annual renewal, rather than a permanent compliance function at the scale of SOX.

The key observation here: SOX compliance for even the smallest public company (under $25M revenue) costs more annually than a SOC 2 Type 2 for most mid-market SaaS companies.

The frameworks are not comparable on cost because they are not comparable in scope. See ComplyJet pricing starting at $4,000 per year, which is less than most companies spend on two weeks of manual compliance prep.

Now that you know what each framework costs, here is what teams get wrong when they try to manage both.

7 SOC 2 vs SOX Mistakes Teams Keep Making in 2026

No competitor article in this space covers mistakes. This section exists because the same seven errors show up across compliance teams at different companies, different stages, and different industries. Avoiding them saves you months of wasted effort.

Mistake 1: Calling SOC 2 a Certification

Your sales team says "we are SOC 2 certified" in the enterprise demo. The procurement lead on the other side of the call knows that is technically wrong. SOC 2 is an attestation. There is no certificate. Say "we have a SOC 2 Type 2 attestation report." That single word change signals framework fluency.

Mistake 2: Submitting SOC 2 Evidence as SOX ICFR Support

SOC 2 covers security controls. SOX auditors testing vendor reliance want SOC 1 reports, not SOC 2 reports. If your public company customer asks for evidence to support their SOX 404 ITGC testing of your platform and you hand them your SOC 2 report, you are giving them the wrong document entirely. They need ICFR-specific assurance that SOC 2 was never designed to provide.

Mistake 3: Assuming Private Companies Have No SOX Exposure

Most Section 404 obligations do not apply to private companies. But Section 806 whistleblower protections extend to contractor employees serving public companies (Lawson v. FMR LLC, Supreme Court, 2014). Section 802 document destruction prohibitions apply broadly. Know what applies to your company before assuming you have zero SOX exposure.

Mistake 4: Reusing SOC 2 Evidence Without Formal SOX Scoping

SOC 2 evidence CAN be reused for SOX ITGC testing. But only for systems where the scope formally overlaps and that overlap is documented. Teams grab SOC 2 access review screenshots for SOX testing without confirming those systems are in scope for financial reporting. External SOX auditors reject undocumented evidence. Align scopes with your SOX auditors before the testing period, not after.

Mistake 5: Starting SOX Readiness in the IPO Year

SOX compliance activates when the registration statement is filed, not when trading begins. Companies that start SOX readiness in the IPO year find themselves building 2 years of controls work into 6 months. EY and Cherry Bekaert both consistently recommend 24 months of preparation before the target IPO date. Start earlier than you think you need to.

Mistake 6: Choosing Privacy Instead of Confidentiality for SOC 2

Many B2B SaaS companies select the Privacy Trust Service Criteria because they process customer data. Privacy is designed for data controllers who interact directly with individuals. Most B2B SaaS companies are data processors, not data controllers. Data processors handling PII on behalf of customers should choose Confidentiality, not Privacy. Privacy is the most resource-intensive TSC category. Choosing it when Confidentiality was the right call adds significant cost and complexity for no additional customer benefit.

Mistake 7: Treating SOC 2 as a One-Time Project

Teams earn their Type 2 report and stop monitoring controls. Then the next audit period starts and controls have drifted. SOC 2 requires continuous control operation throughout the audit period. Evidence must be collected and maintained consistently, not activated 8 weeks before the auditor arrives. According to the CBIZ 2024 SOC Benchmark Study, 92% of organisations conducted at least 2 compliance audits in 2025. Compliance is now a continuous program, not an annual sprint.

Most of these mistakes happen when teams manage compliance manually. ComplyJet automates evidence collection, tracks control health continuously, and alerts you before drift becomes a finding. Start your free trial today.

SOC 2 vs SOX in 2026: What Has Actually Changed

Both frameworks are evolving. The changes in 2025 and 2026 have real implications for how you structure your compliance programs, especially if you are managing both frameworks simultaneously.

Stay ahead of these updates before they create gaps in your current program.

New SOX Rules and Updates Compliance Teams Must Know

The PCAOB is amending AS 2201, the standard governing Section 404 integrated audits, with the amendment effective December 15, 2026 (PCAOB Release No. 2024-005). If you work with a Big 4 firm or any PCAOB-registered auditor, coordinate now on what implementation looks like for your program.

The SEC's 2023 cybersecurity disclosure rules created a new SOX-adjacent obligation. Public companies must disclose material cybersecurity incidents within 4 business days of determining materiality. A security breach affecting financial systems is now both a cybersecurity event and a financial reporting obligation. The SEC's FY2024 enforcement activity saw 583 enforcement actions with a record $8.2 billion in financial remedies. The SEC is pursuing fewer cases but targeting higher-impact outcomes.

AI is also entering SOX programs. Companies using AI in financial processes face emerging ITGC questions. Who controls AI model updates? How are outputs validated before they affect financial data? What change management governs model deployments? These are new ITGC control categories that auditors are beginning to ask about in 2026.

SOC 2 Trends: How the Framework Is Evolving in 2026

The Confidentiality TSC jumped from 34% to 64.4% of all SOC 2 reports in a single year (CBIZ 2024). That surge reflects how many enterprise contracts now explicitly require vendors to make confidentiality commitments. Availability is now in 75.3% of reports, nearly universal.

SOC 2+ reports, which include additional framework mappings such as HITRUST, ISO 27001, or NIST CSF, now represent 9.6% of all SOC 2 reports. Enterprise buyers increasingly want consolidated evidence across frameworks, not separate audits for each. The subservice provider section appears in 89.6% of SOC 2 reports, up from 82% the prior year, which means vendor supply chain scrutiny inside SOC 2 audits is intensifying.

Continuous compliance monitoring is replacing point-in-time evidence snapshots across the industry. If you are still collecting evidence in batches before the audit window, you are already behind how leading compliance teams operate in 2026.

Managing SOC 2 and SOX Together: How Teams Do It Smarter

Running two compliance programs separately is expensive by default. Most teams that manage SOC 2 and SOX as independent programs are collecting the same access review evidence twice, running two sets of control testing, maintaining two evidence libraries, and paying for two audit engagements with no shared work.

There is a better approach, and it starts with recognising that both frameworks are looking at many of the same controls through different lenses.

The Problem: Two Compliance Programs, Double the Work

The overlap identified in the controls mapping section covers access management, change management, system operations, and vendor management. That overlap means duplicated effort in every evidence collection cycle when the two programs are siloed.

Teams running separate programs often discover the problem only when their SOX auditor asks for the same evidence their SOC 2 auditor already collected. At that point, the duplicated work has already happened. The cost and time have already been spent.

The Better Way: One Control Library, Two Frameworks

The solution is mapping shared controls once and collecting evidence once against the mapped controls. A single access review, properly scoped and documented for both SOC 2 CC6 and the SOX access control ITGC, serves both audits simultaneously. A single change approval record covers both CC8 and the SOX change management ITGC on the same systems.

This requires tooling that understands the control mapping between frameworks, not just a spreadsheet. It also requires the scope documentation work described earlier. Done right, SOC 2 and SOX become two lenses on the same control engine, not two separate compliance burdens.

ComplyJet vs Other GRC Tools: What the Difference Looks Like

Most compliance platforms were built for SOC 2 only, or SOX only, or they bolt both together as an expensive add-on. Here is how ComplyJet compares on the dimensions that matter most to teams managing both frameworks.

"We went from manual evidence chaos to automated SOC 2 Type 2 readiness in a week."

That is from Floworks, a YC-backed AI SaaS company with 500 plus customers, who achieved SOC 2 Type 2, ISO 27001, and GDPR compliance on one platform after switching to ComplyJet. Read the Floworks case study to see exactly how they did it.

Start SOC 2 with ComplyJet and reach audit readiness in as little as 2 weeks.

SOC 2 vs SOX: Frequently Asked Questions

Does SOC 2 Cover Financial Reporting Controls?

No. SOC 2 covers operational and security controls across five Trust Services Criteria: Security, Availability, Processing Integrity, Confidentiality, and Privacy. It does not address ICFR. That is SOX's domain. If an enterprise customer asks whether your SOC 2 report covers financial reporting accuracy, the answer is no. That is what SOC 1 is designed for.

Does SOX Cover Cybersecurity?

Not explicitly. SOX was enacted in 2002 before modern cybersecurity frameworks existed. Because financial systems rely on IT infrastructure, cybersecurity controls are essential to SOX IT General Controls. The SEC extended this connection in 2023 with disclosure rules requiring public companies to report material cybersecurity incidents within 4 business days of determining materiality, linking IT security failures directly to financial reporting obligations.

Who Audits SOC 2 vs SOX, and Can It Be the Same Firm?

SOC 2 requires a licensed CPA firm under AICPA SSAE 18, AT-C Section 205. SOX Section 404(b) requires a PCAOB-registered public accounting firm. In practice, both can be performed by the same Big 4 or regional CPA firm, since those firms hold both AICPA membership and PCAOB registration. Independence rules do prohibit firms from providing certain non-audit consulting to the same public company client for whom they provide SOX attestation.

How Long Does a SOC 2 vs SOX Audit Take?

SOC 2 Type 1 takes 3 to 6 months total. SOC 2 Type 2 takes 6 to 15 months, covering a 6 to 12 month observation period plus the audit and reporting phases. A SOX 404 integrated audit runs on the company's fiscal year. The full year is the observation period. Auditors typically begin testing in the second half and issue the report alongside the annual 10-K filing.

How Long Is a SOC 2 Report Valid For?

A SOC 2 Type 2 report covers a defined audit period, typically 6 to 12 months, and documents controls during that time. Enterprise customers typically expect an updated Type 2 report annually. A report older than 12 months is commonly rejected by enterprise procurement teams. Most companies renew on a rolling 12-month basis to maintain continuous coverage.

Is SOC 2 Compliance Mandatory in India?

No. SOC 2 is not legally mandated in India or any other country. It is a US-origin AICPA framework. However, Indian SaaS and IT services companies targeting US and European enterprise customers are increasingly required by those customers to hold a SOC 2 attestation as a contractual condition. The demand is commercial, not regulatory.

Is SOX Compliance Required in India, and What Is India's Equivalent?

US SOX does not apply in India. Indian listed companies are subject to SEBI regulations and India's Companies Act 2013 (Sections 134 and 177), which require management reports on internal financial controls and independent audit committees.

SEBI's Clause 49 of the Listing Agreement introduced board accountability requirements similar in spirit to SOX. India does not have the criminal penalty structure that US SOX carries.

What Are the 4 Pillars of SOX Excellence?

SOX does not formally define four pillars, but compliance practitioners organise SOX excellence around four areas aligned to the COSO framework: Control Environment (governance and ethical culture), Risk Assessment (identifying material financial reporting risks), Control Activities (specific IT and process controls that mitigate those risks), and Continuous Monitoring (ongoing evaluation of control effectiveness beyond annual testing cycles).

What Is J-SOX, and How Does It Compare to US SOX?

J-SOX refers to Japan's Financial Instruments and Exchange Act, enacted in 2006 after corporate scandals including Seibu Railway and Livedoor. Like US SOX, it requires management assessment of internal controls over financial reporting and external auditor attestation. Key differences: J-SOX applies only to Tokyo Stock Exchange-listed companies and sets revenue thresholds above which full ICFR attestation is required. US SOX applies to all SEC-listed companies regardless of size, with limited filer category exemptions for 404(b) attestation only.

Does SOX Apply in the UK?

US SOX does not apply to UK-domiciled companies listed only on UK exchanges. UK companies listed on US exchanges as foreign private issuers must comply with modified SOX requirements. The UK Corporate Governance Code, updated in January 2025, now requires UK-listed companies to make annual statements on the effectiveness of their internal controls, bringing the UK functionally closer to SOX 404 obligations. Directors of UK-listed companies are personally responsible for material financial irregularities under UK law.

What Are the SOX Data Retention Requirements?

Under SOX Section 802 and SEC Rule 2-06 (17 CFR 210.2-06), audit workpapers and all related records, including memoranda, correspondence, and electronic records containing conclusions, analyses, or financial data related to an audit, must be retained for a minimum of 7 years. Knowingly destroying, altering, or concealing records relevant to a federal investigation carries up to 20 years imprisonment. This applies to both audit firms and the audited companies.

Is ISO 27001 Harder to Achieve Than SOC 2?

Neither is inherently harder. They have different structures. ISO 27001 is a true certification covering 93 controls across 4 themes, requiring an Information Security Management System.

SOC 2 Type 2 requires sustained evidence of control operation over 6 to 12 months. Companies pursuing both often find 30 to 40% evidence overlap. According to the CBIZ 2024 SOC Benchmark Study, 81% of organisations planned ISO 27001 certification in 2025, up from 67% in 2024, reflecting increasing demand for multi-framework coverage.

Is There a SOC 3 Report, and How Is It Different From SOC 2?

Yes. SOC 3 is an AICPA report based on the same Trust Services Criteria as SOC 2, but designed for public use. It can be freely published on your website.

Unlike SOC 2, SOC 3 omits detailed control descriptions, testing procedures, and audit exceptions. It includes only the auditor's opinion and management's assertion. SOC 3 is a useful public trust signal but does not satisfy enterprise procurement teams who need the full SOC 2 report detail for their vendor risk programs.

What Is the 5% Materiality Rule in SOX?

SOX does not define a specific percentage for materiality. By common accounting practice, a misstatement may be considered material if it exceeds 5% of pre-tax income or 0.5% of total assets. These are rules of thumb, not legal thresholds.

Under PCAOB AS 2201, a material weakness exists when there is a reasonable possibility that a material misstatement of the financial statements would not be prevented or detected. Auditors assess materiality both quantitatively and qualitatively.

What Is the ICFR vs SOX Relationship?

ICFR (Internal Control over Financial Reporting) is not a separate framework. It is the subject of SOX. SOX Section 404 requires management to assess ICFR effectiveness annually. Section 404(b) requires an external auditor to attest to that assessment for larger filers.

SOX is the legal mandate. ICFR is what the mandate requires you to have, maintain, and evaluate. The COSO framework is most widely used to design and assess ICFR under SOX.

SOC 2 vs SOX: Two Different Frameworks, One Decision

Back to that Thursday conference room. Team Finance now has its SOX ICFR evidence pack. Team Engineering has its SOC 2 Type 2 attestation report. The answer to the question is clear: you cannot give your SOX auditors your SOC 2 report as ICFR evidence. They are built for different masters, answering to different audiences, under different rules.

But the overlap of the controls is real. The scoping path exists. When you are ready to optimise, the two frameworks can share evidence, reduce duplication, and run as one unified compliance program instead of two separate burdens.

The SOC 2 vs SOX question does not have a single answer. It depends entirely on who you are answering to: your customers, your regulators, or both. Once you know that, the rest is execution.

For SaaS teams beginning their SOC 2 compliance program, ComplyJet is built to get you there without the manual overhead. Plans start at $4,000 per year. Audit readiness in as little as 2 weeks. Book your free demo today!